South Carolina Uninsured & Underinsured Motorist (UM/UIM) Coverage Explained

Car Accidents in Upstate South Carolina and the Insurance Problem

Car accidents across Upstate South Carolina - including Greenville, Spartanburg, Anderson, Easley, and surrounding areas - often involve a frustrating reality: many drivers do not carry enough insurance to fully cover the harm they cause.

Some drivers have no insurance at all. Others carry only the minimum required coverage, which is often not enough after a serious crash involving medical treatment, lost wages, or long-term injury.

When that happens, injured individuals are often left with a critical question: who is responsible for paying the remaining damages?

That is where Uninsured Motorist (UM) and Underinsured Motorist (UIM) coverage come in.

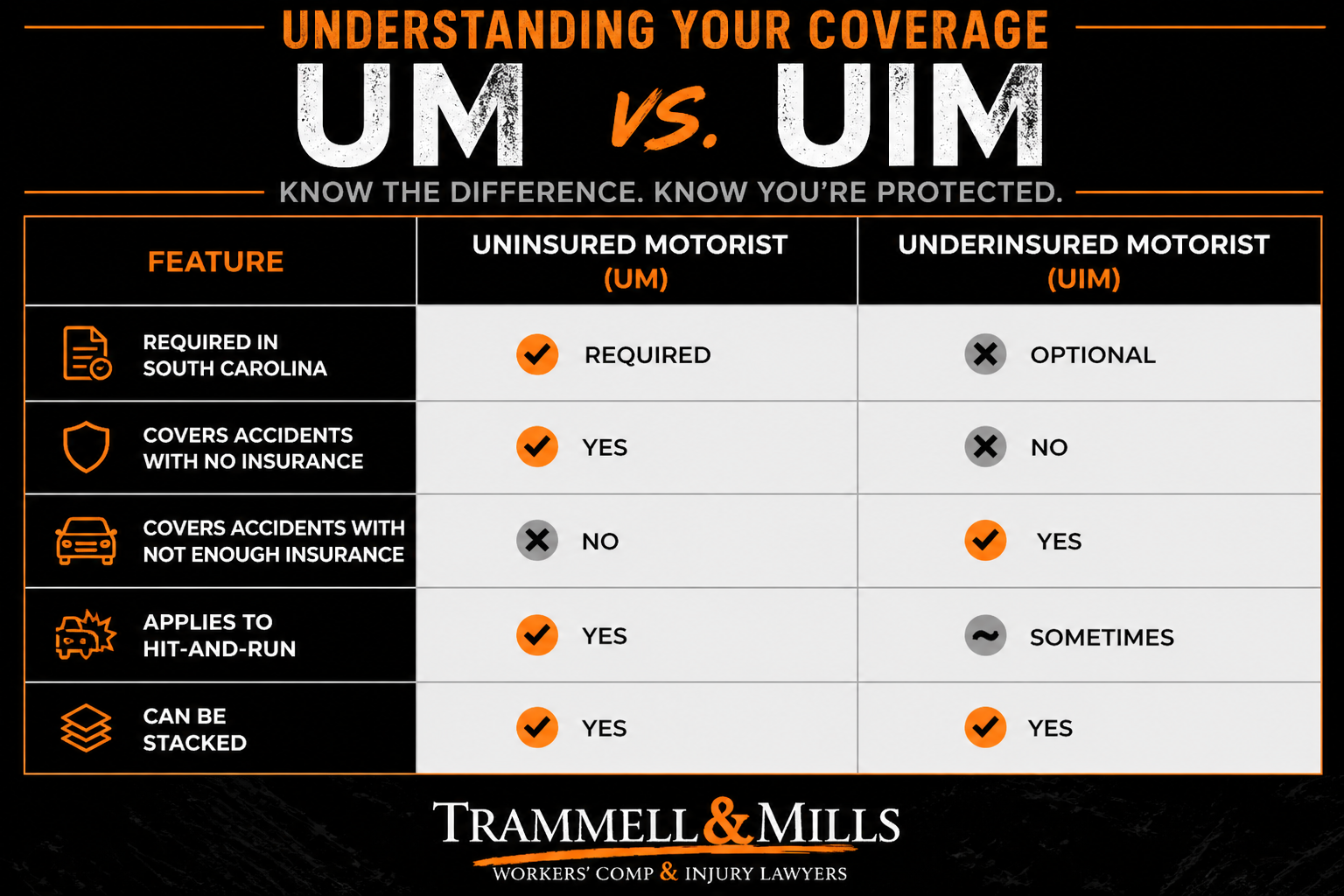

What Is Uninsured Motorist (UM) Coverage in South Carolina?

Uninsured Motorist coverage protects you when the at-fault driver has no insurance or cannot be identified after a hit-and-run accident.

In South Carolina, UM coverage is required on all auto insurance policies. In practice, it means your own insurance steps in when the at-fault driver cannot pay.

In hit-and-run cases, UM coverage is often the only available source of recovery.

What Is Underinsured Motorist (UIM) Coverage?

Underinsured Motorist coverage applies when the at-fault driver has insurance, but not enough to cover your total damages.

This is extremely common in Upstate South Carolina, where many drivers carry minimum liability limits that can be exhausted quickly in even moderate injury cases.

These minimum limits are:

- $25,000 bodily injury coverage per person

- $50,000 bodily injury coverage per accident

- $25,000 property damage coverage

For example, if:

- At-fault driver insurance: $25,000

- Your total damages: $100,000

When you recover the at fault party's full policy limits, UIM coverage may help cover the remaining losses, depending on your policy limits.

Unlike UM coverage, UIM is not required in South Carolina, but insurers must offer it when you purchase coverage. It only applies when the at fault party's insurance policy is is tendered and exhausted. In other words, it is "excess coverage" that bridge the gap between your losses and the at-fault driver's insurance limits.

Underinsured motorist coverage is not something worth excluding. It exists solely to protect you and your passengers by covering damages you’re legally entitled to recover when the at-fault driver’s insurance limits are insufficient to fully compensate you. Without UIM coverage, victims are often left undercompensated.

Can You Stack UM/UIM Coverage in South Carolina?

South Carolina allows “stacking” of Uninsured Motorist and Underinsured Motorist coverage in many situations. Stacking means you can combine coverage limits to increase the total amount available after a serious accident.

This can apply in two ways:

- Stacking multiple vehicles on the same insurance policy

- Stacking across multiple separate policies (in certain situations)

When stacking is allowed, it can significantly increase the total recovery available if the at-fault driver’s insurance is not enough to fully compensate your damages.

How stacking depends on your classification: Class I vs. Class II insureds:

South Carolina divides insured individuals into two categories, which largely determines stacking rights:

Class I insureds (broader rights / stacking usually allowed) include:

- The named insured on the policy

- The spouse of the named insured residing in the same household

- Resident relatives (family members living in the same household)

Class I insureds generally have the strongest UM/UIM protections. They are often allowed to stack coverage across multiple vehicles on a policy, and in some cases across multiple policies, depending on the facts and policy structure.

Class II insureds (limited rights / usually no stacking) include:

- Permissive drivers (someone driving the insured vehicle with permission)

- Passengers who are not named insureds or resident relatives

Class II insureds are typically limited to the coverage on the specific vehicle involved in the accident and usually cannot stack additional UM/UIM limits from other vehicles or policies.

How a Greenville and Upstate SC Car Accident Lawyer Can Help

Handling a UM/UIM claim involves more than filing paperwork.

A lawyer can:

- Identify all available insurance coverage

- Determine whether stacking applies

- Negotiate with your insurance carrier

- Document the full extent of your injuries

- Pursue maximum compensation under SC law

In serious injury cases, this can make a substantial difference in recovery.

Contact Trammell & Mills Law Firm

If you were injured in a car accident in Upstate South Carolina involving an uninsured or underinsured driver, Trammell & Mills Law Firm can help you evaluate your UM/UIM coverage and pursue full compensation.

Call Trammell & Mills Law Firm today for a free consultation to evaluate your UM/UIM coverage and legal options.

Share On: